UK Savings Week, a fantastic awareness campaign designed to encourage positive attitudes towards saving and to help those around the UK to enhance their financial resilience, takes place between 18 and 24 September 2023.

Considering that the website reveals that around 11.5 million people in the UK have less than £100 of savings to fall back on in an emergency, it’s an important initiative.

Whether you’re saving towards the deposit for a home, building your emergency fund, or bolstering your retirement savings, it can sometimes be easier said than done to set money aside for your future.

So, with UK Savings Week here, it’s an ideal time to review some helpful ways to boost your savings – continue reading to discover five useful tips.

1. Set achievable goals

Establishing realistic savings goals is a vital step to ensure that you maintain your motivation and stick to your targets. For instance, if you would struggle to set aside £200 each month, it may be unwise to suddenly set yourself a monthly saving target of £500.

It’s also beneficial to focus on specific milestones, such as a home deposit or building a comfortable retirement fund. On top of this, it may be prudent to set a savings deadline, helping you create a structured schedule for your efforts.

Not only could this make your savings goals more tangible, but it could also help you figure out how much you realistically need to save each month.

2. Reassess your spending and budget

An excellent way to find extra cash to boost your savings is by revisiting your budget and current expenditure.

Start by examining your bank statements and take note of all your outgoings and financial commitments. Once you’ve calculated your monthly expenses, you can assess your remaining income and determine where you could save some money.

For example, you may discover unused subscriptions you can cancel, such as streaming services or gym memberships.

Even a few spare pounds saved each month could go a long way in helping you feel more financially secure.

3. Pay your future self first

A common approach to saving is to wait until the end of the month to assess what you have left in your bank account, then save those funds.

However, a more proactive strategy to boost your savings could be to pay your future self first. This is essentially when you do the opposite and make any savings contributions immediately after pay day, then budget your monthly expenses based on what you have left.

Doing so could remove the temptation to skip a contribution at the end of a month and spend the money on other discretionary items.

After trying this for some time, you could increase the amount you put aside each month in small increments. This could boost your savings while still leaving yourself with enough cash to enjoy your life and live your desired lifestyle.

4. Visualise your savings milestones

Perhaps one of the better ways to boost your savings, feel motivated, and maintain your willpower, is to picture what it is you’re saving for.

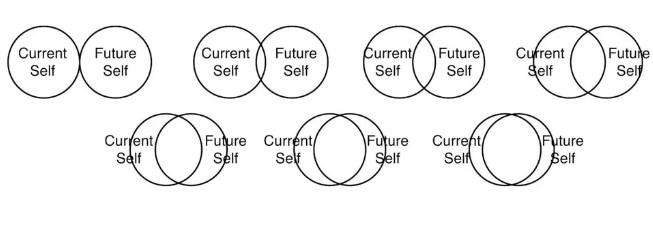

In a study reported by the BBC, a professor showed participants a graph revealing pairs of circles representing their current and future selves. The participants then had to identify which pair of circles best described how similar and connected they felt to their future selves 10 years from then.

Source: BBC

The participants who felt a greater connection to their future selves – those who had far more precise plans about what they wanted to do in 10 years’ time – had more savings than those who lived in the present.

As such, it’s worth approaching your savings goals by thinking about what you want to achieve in the future. You should ideally consider what you’re saving for, rather than just saving for the purpose of accumulating wealth.

This could help you focus your mind and stick to your savings plan, keeping the motivation alive in your mind.

5. Make the most of tax-efficient savings

More practically, using tax-efficient savings vehicles could significantly boost your wealth. Even if you can’t generate more surplus cash to save each month, making the most of the savings you do have is key.

For instance, if you make pension contributions, you can benefit from an immediate boost of 20%, 40%, or 45% from tax relief, depending on your marginal Income Tax rate. This means that if you’re a higher-rate taxpayer and make a £100 contribution, this only “costs” you £60 due to the 40% tax relief.

Similarly, ISAs are another practical way to save tax-efficiently, as the returns on ISAs are entirely free from Income Tax and Capital Gains Tax.

Moreover, if you’re saving the deposit for your first home, a Lifetime ISA allows you to deposit £4,000 a year and earn an additional 25% bonus from the government on contributions. As such, you could benefit from an extra £1,000 of savings on a £4,000 contribution.

However, it’s important to note that you will typically face a withdrawal penalty if you attempt to use the money within your Lifetime ISA before age 60 for anything other than the deposit for your first home.

Get in touch

If you wish to take control of your finances, or even set savings goals that you can realistically achieve, then we could help.

Please email enquire@london-money.co.uk or call (0207) 808 4120 to find out more.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.