There’s a good chance you’ve seen that mortgage rates have risen substantially in the last few months. In fact, This is Money reports that more than 1.4 million people in the UK could face a significant increase in their repayments in 2023 as their fixed-rate deals come to an end.

The same source states that more than half (57%) of deals coming up for renewal this year are at rates lower than 2%. Meanwhile, the average two-year fixed rate now stands at 5.75%, while the average five-year fixed-rate deal stands at 5.57%.

One of the ways that could help you reduce your monthly repayments is an offset mortgage. This is essentially when you link your savings to your mortgage, “offsetting” the balance between the two.

So, how exactly does an offset mortgage work? And could it really help you reduce your monthly repayments? Continue reading to discover everything you need to know.

An offset mortgage allows you to reduce the interest you pay each month by linking your savings

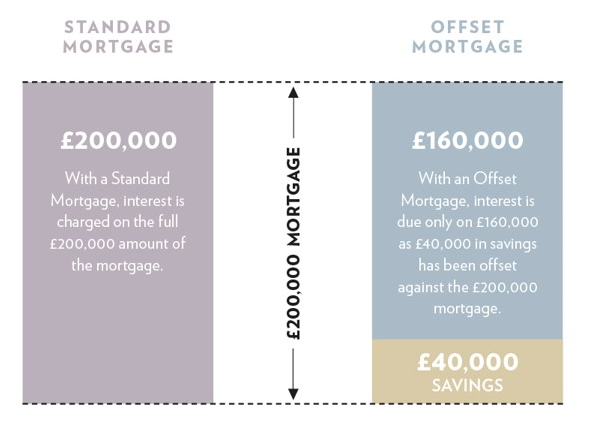

An “offset mortgage” is a type of property loan that links a savings or current account to your mortgage. Then, the money you hold in your linked account is used to reduce the total balance you pay interest on every month.

The amount you owe is “offset” by the balance of your linked account, and the interest is calculated on the difference between the two.

With a typical mortgage, you borrow a lump sum and make monthly payments to repay the loan. These repayments normally include some of the amount you borrowed, and interest.

Meanwhile, with an offset mortgage, the amount you have in savings is treated much like “credit” on your mortgage, almost like an overpayment.

It’s worth noting that your savings are only used to offset the remaining balance for interest reasons; you’ll still need to pay off the entire loan.

Source: Family Building Society

The infographic above, shows exactly how offset mortgages work.

As for their rates, This is Money reports that the average rate on an offset mortgage as of 15 March 2023 was 5.45%. Compare this to the average two-year fixed rate of 5.32% and the average five-year fixed rate of 5%.

Even though offset mortgage rates are slightly higher than their two- and five-year fixed-rate counterparts, if you have savings that aren’t generating a return equivalent to that of your mortgage rate after tax, they may still be worth considering.

The benefits of an offset mortgage

Perhaps the most significant benefit of an offset mortgage is that you can save money by paying a reduced amount of interest on your mortgage.

Family Building Society gives a great example of how much you could save with an offset mortgage. If you have a standard £200,000, 30-year capital and interest mortgage with a rate of 2.19%, you will pay back £758.39 each month.

Meanwhile, if you have an offset mortgage and have £40,000 saved in your linked account, you would only be paying £685.39 monthly – a £73 saving.

Alternatively, you can maintain your mortgage repayment at the same amount. This would have the effect of repaying your mortgage more quickly. In the example above, you would repay your mortgage four years earlier if you maintain your repayments at the higher amount.

An offset mortgage could be perfect if you have cash saved, but the savings aren’t working for you. If you have surplus cash, it could be used to reduce the interest you pay on your mortgage.

It could also be perfect if you have raised money for something like a home renovation where the funds won’t be fully required immediately. You can then offset this money against your mortgage to help reduce your costs or term until you need the funds.

Some important things to consider about offset mortgages

If you’re considering an offset mortgage you should bear in mind that you may pay a higher interest rate. As you read above, offset mortgages tend to have higher initial rates than their traditional counterparts, which means your standard monthly repayments may not be as low as a traditional deal.

Also, you typically don’t earn interest on the savings in your account that you used to offset the mortgage. The money is used to reduce interest costs on the debt, so you won’t see your savings grow as if you’d left them in a savings account or Cash ISA.

This is why it may be wise to speak with us before getting an offset mortgage. We can help you consider the various options to see whether an offset or traditional mortgage would most benefit you.

Get in touch

Offset mortgages are just one of many ways to potentially reduce your monthly outgoings amid times of high mortgage rates.

To discuss this more, please email enquire@london-money.co.uk or call (0207) 808 4120.

Please note

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it. Think carefully before securing other debts against your home.