If you’ve been on the hunt for a new mortgage deal in recent months, you’ll have likely seen that the mortgage market was uncertain in the final months of 2022, with many lenders significantly increasing the cost of borrowing.

In fact, many lenders in the UK gradually increased rates over the course of last year in line with the Bank of England (BoE) base rate, which stands at 4% as of 1 March 2023. This is the highest the base rate has been in 14 years.

Despite this, FTAdviser reports that the cost of fixed-rate mortgages has started to fall after peaking at 6% last year. Keep reading to discover why mortgage rates rose so much last year, and some predictions of how they could move in 2023.

Mortgage rates climbed in 2022 due to base rate hikes and the mini-Budget

As you may have seen, mortgage rates rose significantly at the end of 2022. FTAdviser reports that the average interest rate on a two-year fixed-rate mortgage increased from 2.52% to 5.79% between January 2021 and mid-January 2023.

This can be partly attributed to the fact that the BoE increased the base rate several times in 2022 in an attempt to combat inflation. The base rate rose from 0.25% on 28 January 2022 to 3.5% by 21 December of the same year.

Now, the base rate stands at 4% as of 1 March 2023, and, according to the BBC, experts predict this to peak at 4.5% this summer.

Also, the mini-Budget in September resulted in volatility in the mortgage market. In fact, the Guardian reports that more than 40% of mortgage deals disappeared overnight following Kwasi Kwarteng’s statement.

Of course, the reversal of many of the decisions announced in the mini-Budget calmed mortgage markets significantly. So, will this trend continue into 2023?

Some experts predict that mortgage rates could decline throughout 2023

Many lenders have eased mortgage rates since they peaked in October 2022, though they remain relatively high compared to the historic lows during the Covid-19 pandemic.

As of 1 March 2023, Moneyfacts reports that the lowest two-year fixed-rate capital and interest mortgage on the market for someone purchasing a new home stands at 4.54%.

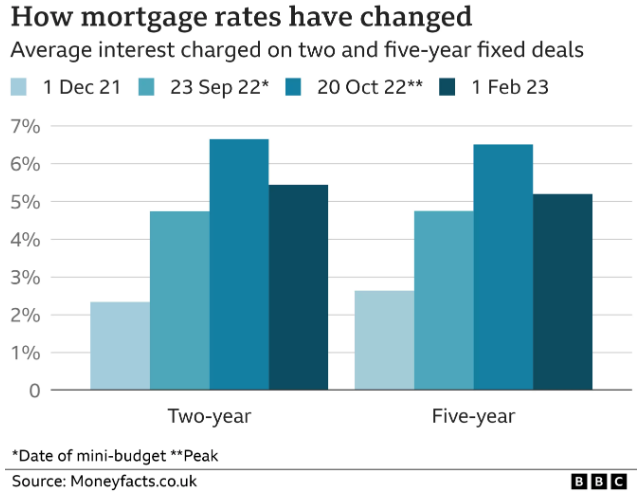

The above chart, which was sourced from the BBC, shows how mortgage rates have changed since 1 December 2021. While costs are still much higher when compared with December 2021, you can see that they’ve started to fall since peaking in October 2022.

Many experts believe that rates will continue to decline gradually through 2023. If the base rate peaks at its current level, lenders may be able to maintain the mortgage deals already on offer, or even lower prices.

In fact, the Guardian reports that five-year fixed-rate mortgages recently fell below 4% for the first time since the mini-Budget, which could potentially be a good sign for the overall mortgage market.

Despite many experts taking a positive outlook, it’s worth noting that mortgage approvals remain low. Sky News states that the base rate hikes have caused mortgage approvals to drop to their lowest level since before lockdowns, falling to 35,600 in December 2022. This is the lowest mortgage approvals have been since May 2020.

You should remember that it’s near impossible to accurately predict how mortgage markets will move. That’s why you should ideally work with a mortgage broker who can help you secure a mortgage deal quickly and efficiently and relieve some of the stress of finding a mortgage.

Better yet, mortgage brokers can often access deals that aren’t usually available to the public, and you could get a fantastic deal on your mortgage as a result.

Get in touch

While it’s near impossible to predict precisely how mortgage rates may move in 2023, we can help alleviate some of the stress involved with securing a deal.

Please email enquire@london-money.co.uk or call (0207) 808 4120 to find out more.

Please note

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.